Gift Letter for Mortgage

A Gift Letter for Mortgage is a legal instrument that formally confirms a monetary gift intended for a mortgage down payment, affirming no expectation of repayment.

Relationship To Borrower

Select the relationship between the person giving the gift and the person receiving it. Lenders require this information to verify the legitimacy of the gift.

Provide details if you selected 'Other'.

Table of Contents

What is a Gift Letter for Mortgage?

A Gift Letter for Mortgage is a formal document used in real estate transactions when a portion of the funds for a down payment or closing costs is provided by a third party as a gift, rather than a loan. This letter serves as official confirmation to a mortgage lender that the funds are a true gift and do not need to be repaid. Its primary purpose is to assure the lender that the borrower’s debt-to-income ratio will not be adversely affected by an undisclosed loan, which is crucial for underwriting the mortgage.

Purpose and Significance in Mortgage Lending

In the mortgage application process, lenders meticulously assess a borrower's financial capacity, including their income, assets, and liabilities. When a borrower receives financial assistance for a down payment or closing costs from another individual, lenders need to understand the nature of these funds. A Gift Letter for Mortgage is vital because it clarifies that these funds are not a loan that would add to the borrower's debt burden. Without this letter, lenders might view such funds as an unrecorded debt, potentially impacting the borrower’s eligibility for the mortgage.

This document helps maintain transparency and integrity in the lending process. It provides assurance that the borrower's financial stability, as presented in their application, is accurate and not predicated on obligations that are not disclosed. The letter is a key component in demonstrating the legitimate source of funds, thereby complying with anti-money laundering regulations and ensuring the overall financial health of the transaction.

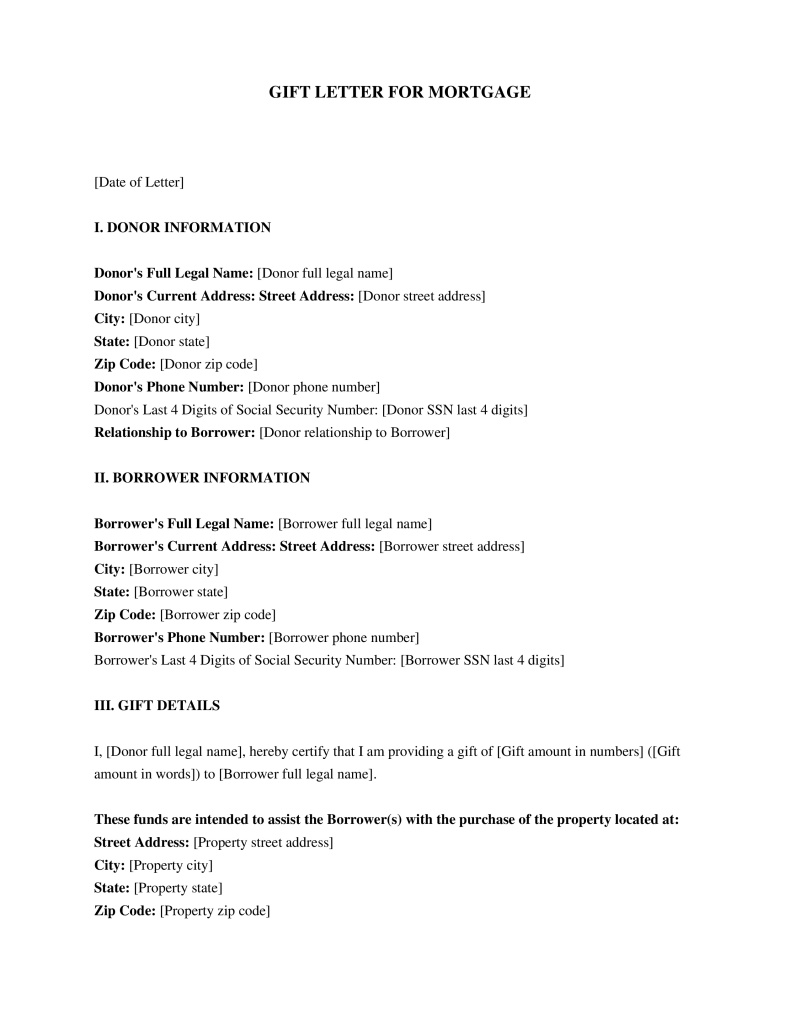

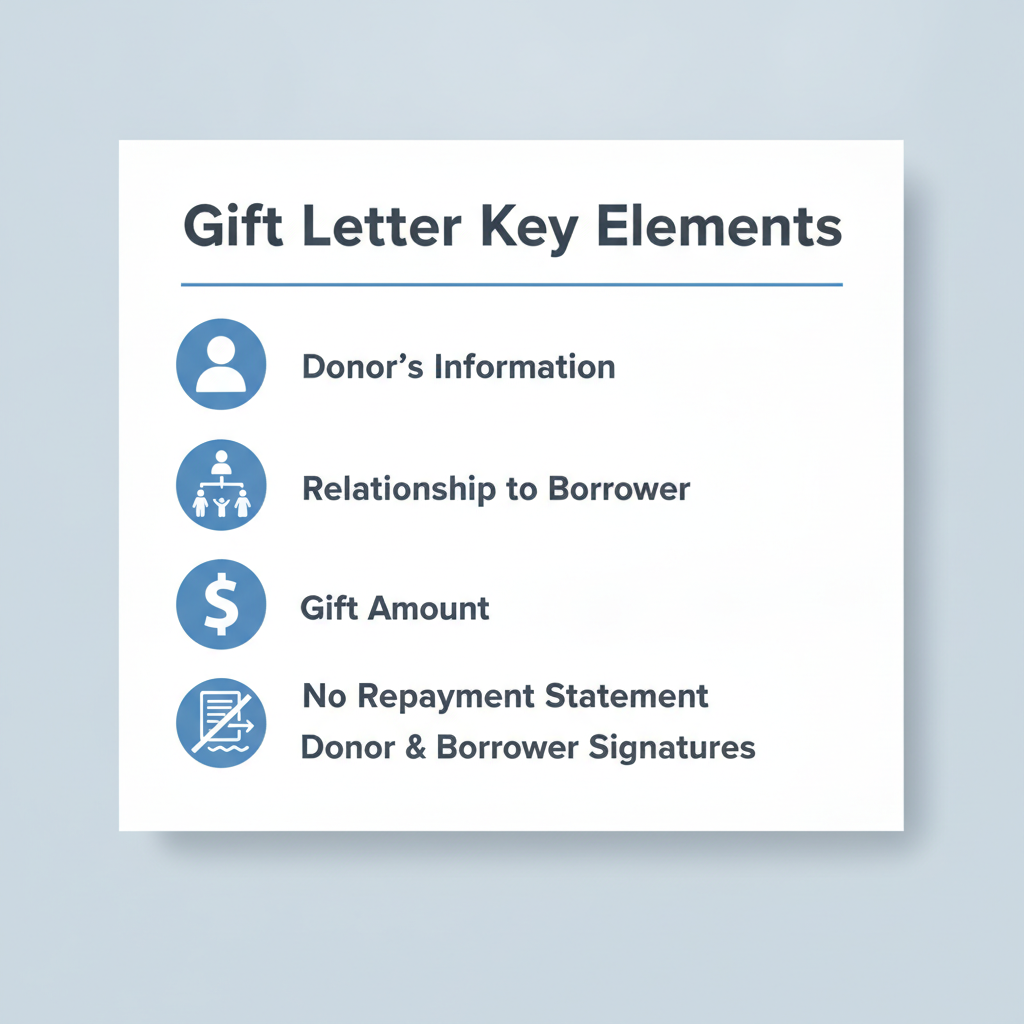

Essential Elements of a Gift Letter

Mortgage lenders, particularly for government-backed loans such as those insured by the Federal Housing Administration (FHA), require specific information to be included in a Gift Letter for Mortgage. The mortgagee must obtain a gift letter that is signed and dated by both the donor and the borrower. This letter must contain several key details to be considered valid for mortgage underwriting purposes:

- Donor's Information - The full name, current address, and telephone number of the individual providing the gift.

- Relationship to Borrower - A clear statement detailing the donor's relationship to the borrower, such as parent, grandparent, or other close relative.

- Gift Amount - The exact dollar amount of the gift being provided for the mortgage transaction.

- No Repayment Statement - An explicit statement from the donor affirming that the funds are a gift and no repayment is expected or required (HUD Handbook 4000.1, HUD 4155.1).

- Donor and Borrower Signatures - The signatures of both the donor and the borrower, along with the date of signing.

These elements ensure that the letter provides a comprehensive and unambiguous declaration of the gift, satisfying lender requirements and regulatory guidelines.

Donor Eligibility and Relationship Requirements

While the concept of a gift for a mortgage is straightforward, specific rules often govern who can provide such a gift. Lenders typically prefer gifts from close relatives to minimize the risk of undisclosed repayment expectations or fraudulent activity. The relationship between the donor and the borrower is a critical piece of information required in the gift letter.

Generally, acceptable donors include immediate family members, such as parents, grandparents, siblings, or spouses. In some cases, employers or charitable organizations may also be permitted to provide gift funds, though these situations often come with additional scrutiny or specific program requirements. The clear identification of the donor's relationship to the borrower in the gift letter helps lenders assess the legitimacy and intent behind the gift, ensuring it aligns with their underwriting standards.

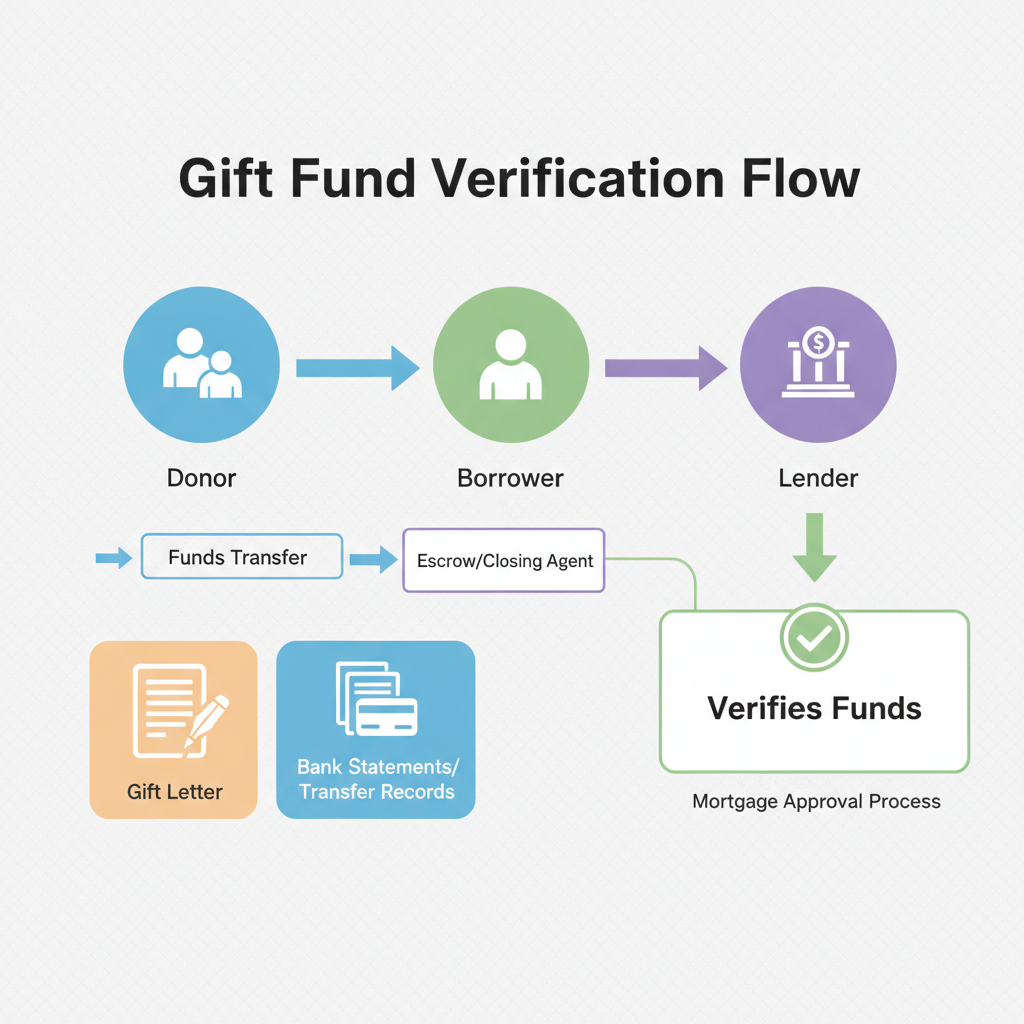

Documentation and Verification of Gift Funds

Beyond the gift letter itself, lenders require documentation to verify the transfer and availability of the gift funds. This process ensures that the funds genuinely exist and have been moved from the donor to the borrower or directly to the closing agent.

The required documentation typically includes:

- Donor's Bank Statement - A copy of the donor's bank statement showing the withdrawal of the gift funds.

- Borrower's Bank Statement - A copy of the borrower's bank statement showing the deposit of the gift funds.

- Transfer Records - A copy of the canceled check, wire transfer confirmation, or other official transaction records demonstrating the movement of funds from the donor to the borrower's account or directly to the escrow agent (HUD 4155.1).

- Letter of Explanation (if needed) - If there are any unusual circumstances or delays in the transfer, a letter of explanation may be required from either the donor or borrower.

This verification process is essential for preventing fraud and confirming that the gifted funds are legitimate and fully accessible for the mortgage transaction.

Implications of Repayment Clauses

A fundamental principle of the Gift Letter for Mortgage is the explicit statement that no repayment is required. This clause is not merely a formality; it carries significant implications for both the borrower and the lender. If there were any expectation of repayment, the funds would be considered a loan, not a gift. This reclassification would alter the borrower’s debt-to-income ratio, potentially disqualifying them for the mortgage or requiring a restructuring of the loan terms.

Lenders rely on the gift letter to accurately reflect the borrower's financial obligations. Any indication of a repayment agreement, even an informal one, can lead to the rejection of the mortgage application. The statement of no repayment protects the lender from unforeseen liabilities and ensures that the borrower's ability to repay their mortgage is not compromised by hidden debts to the gift donor.

Frequently Asked Questions

Sources

- HUD Handbook 4000.1: FHA Single Family Housing Policy Handbook - Provides detailed requirements for gift letters in FHA-insured mortgages, including necessary information and documentation.

- HUD 4155.1: Handbook for Lenders on Underwriting and Processing Mortgages - Outlines the required documentation for gift funds, including the gift letter and verification of fund transfer.

Not the form you're looking for?

Try our legal document generator to create a custom document

Disclaimer: The templates available on this website are provided for general informational purposes only and do not constitute legal advice. They are not intended to be, and should not be interpreted as, compliant with any specific legal, regulatory, or privacy requirements. These templates are not a replacement for professional legal guidance and should not be relied upon for any particular matter or circumstance. Users are strongly encouraged to seek advice from a qualified attorney licensed in their jurisdiction before using, modifying, or relying on any template.

All templates are provided on an "as is," "with all faults," and "as available" basis. The provider disclaims any and all warranties of any kind, whether express, implied, statutory, or otherwise, including without limitation warranties of merchantability, fitness for a particular purpose, title, or non-infringement.

LegalTemplates.com makes no guarantees or representations regarding the accuracy, completeness, expected outcomes, or reliability of the materials contained in these templates or any materials referenced or linked from them.