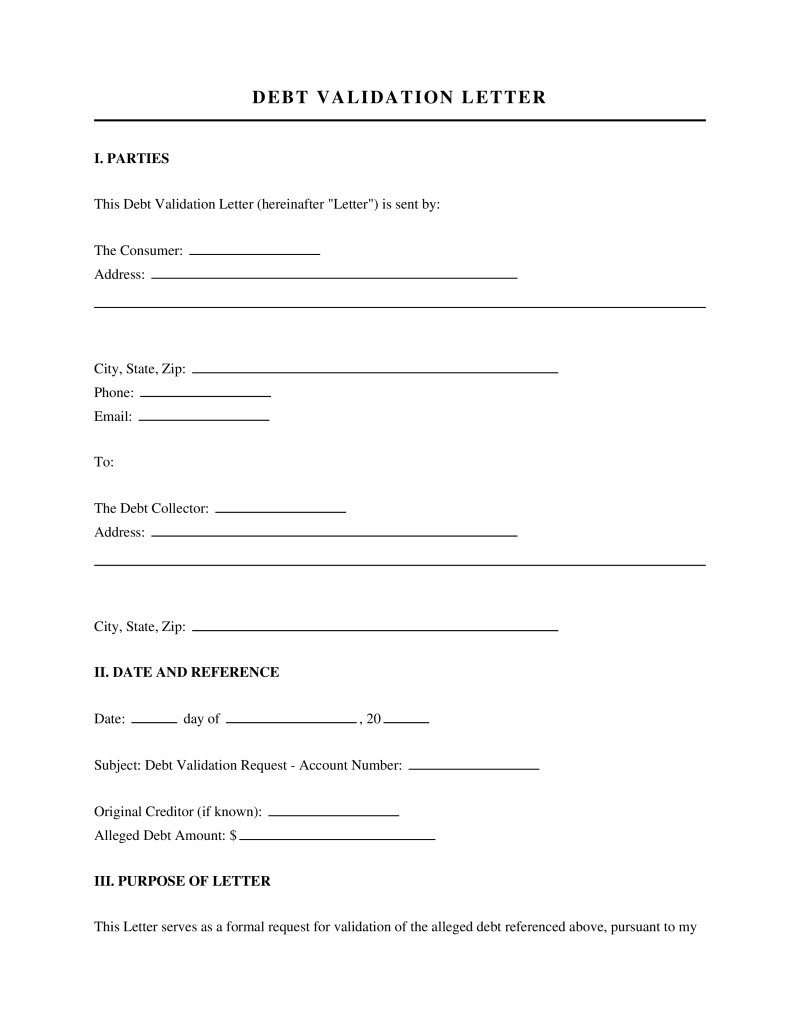

Debt Validation Letter

A Debt Validation Letter is a formal legal document sent to a debt collector, challenging the validity of an alleged debt and requesting substantiating.

Debt Collector Type

Choose whether the debt collector is an individual (a single person) or a business entity (a company or organization). This information helps determine the legal obligations and protections you may have in your situation. Select the option that best fits the debt collector you are dealing with.

Enter the name of the individual or authorized representative.

Enter the full legal name of the debt collection agency.

Provide the official mailing address of the debt collector.

Enter a contact phone number for the debt collector (optional).

Table of Contents

What is a Debt Validation Letter?

A Debt Validation Letter is a formal written request sent by a consumer to a debt collector to demand proof that a claimed debt is legitimate and that the collector has the legal right to collect it. This letter is a crucial tool under federal consumer protection laws, particularly the Fair Debt Collection Practices Act (FDCPA), enabling individuals to challenge the accuracy or ownership of a debt. Its primary purpose is to protect consumers from erroneous claims, fraudulent debts, or collection attempts by parties without proper authority.

The Right to Debt Validation

Consumers have a legal right to request validation of a debt they are being asked to pay. This right is established to ensure fairness and transparency in debt collection practices, preventing collectors from pursuing debts without proper substantiation. The debt collector is obligated to provide specific information about the debt to the consumer.

- Initial Communication Requirement - A debt collector must provide validation information either during their first communication with a consumer or within five days of that initial communication (Consumer Financial Protection Bureau).

- Consumer's Right to Dispute - After receiving the validation information, a consumer has a 30-day period during which they can dispute the debt or request additional information.

- Cessation of Collection Activities - If a consumer sends a written request for validation within this 30-day window, the debt collector must cease all collection efforts until they have provided the requested validation information.

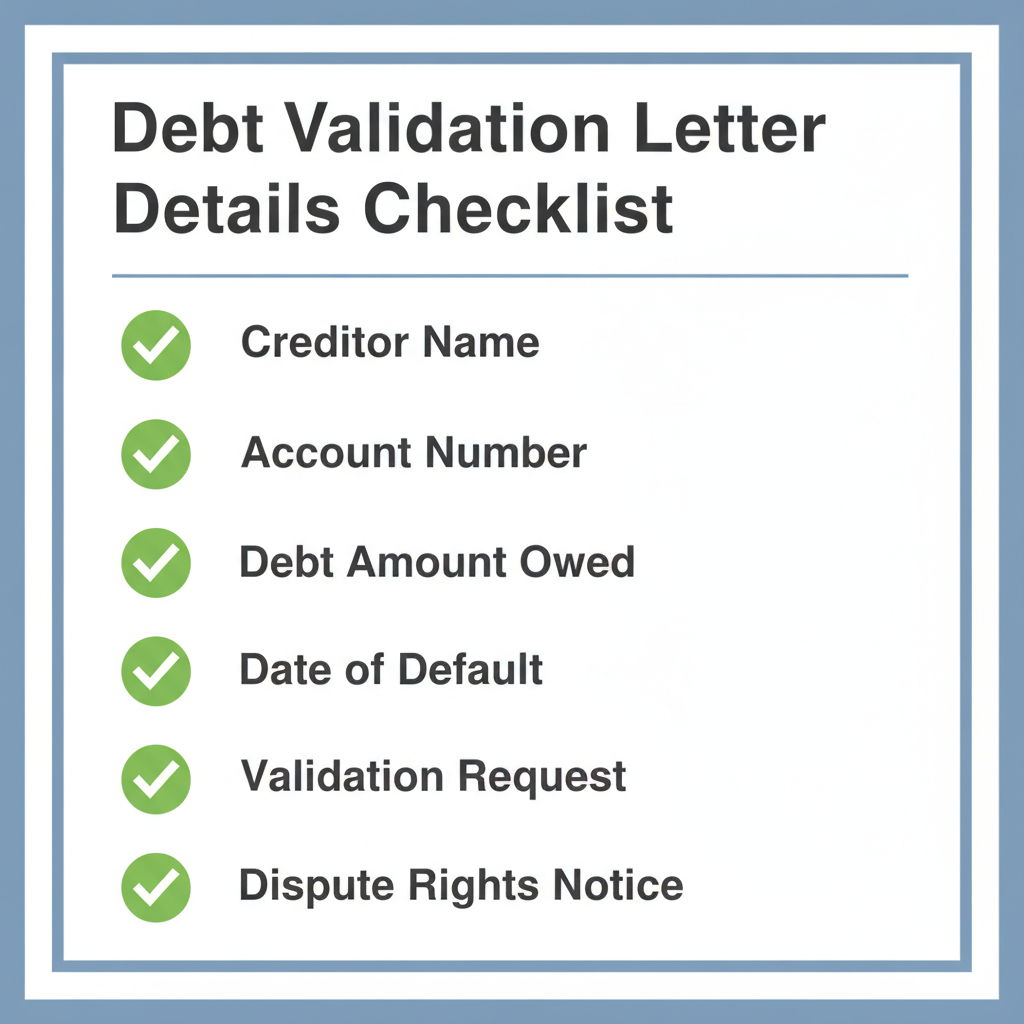

Required Validation Information from Debt Collectors

Debt collectors are required to provide specific details about the debt they are attempting to collect. This information, often referred to as validation information, ensures that consumers can accurately identify the debt and understand their rights regarding it. The Debt Collection Rule mandates that collectors provide five categories of validation information.

- Debt-Related Information - This includes the name of the creditor to whom the debt is currently owed, the amount of the debt, and an itemization of the current amount of the debt (Consumer Financial Protection Bureau).

- Itemization of Debt - The itemization must show the principal amount, any interest, fees, payments, and credits since the last payment or credit (Consumer Financial Protection Bureau).

- Consumer Protections Information - Details about the consumer's rights under the Fair Debt Collection Practices Act (FDCPA), including the right to dispute the debt within 30 days (Federal Trade Commission).

- Clear Dispute Instructions - A statement explaining that the consumer can dispute the debt in writing within 30 days after receiving the validation information (Federal Trade Commission).

- Collector's Identification - The name of the debt collector and the mailing address and telephone number at which the debt collector can be reached (Federal Trade Commission).

When to Send a Debt Validation Letter

The timing of sending a Debt Validation Letter is critical to maximizing its protective benefits under federal law. Consumers should act promptly upon receiving initial communication from a debt collector regarding a debt they believe may be inaccurate or unfamiliar.

- Within 30 Days of Initial Contact - A consumer should send a Debt Validation Letter within 30 days of receiving the initial validation notice from the debt collector. This 30-day period is crucial because it triggers specific protections under the FDCPA.

- Effect of Timely Request - If a consumer sends a written validation request within this 30-day period, the debt collector must stop all collection activities until they provide the requested validation information. This includes refraining from making phone calls, sending letters, or reporting the debt to credit bureaus.

- After 30 Days - While consumers can still send a Debt Validation Letter after the 30-day window, the debt collector is not legally obligated to cease collection activities until validation is provided. However, the collector may still choose to validate the debt.

Contents of a Consumer's Debt Validation Letter

A consumer's Debt Validation Letter should be clear, concise, and formally request the specific information needed to verify the debt. While no specific legal template is required, certain elements are typically included to ensure its effectiveness.

- Identification of Debt - The letter should clearly state the account number or other identifying information provided by the debt collector, allowing them to easily identify the specific debt in question.

- Request for Validation - The core of the letter is a clear statement requesting validation of the debt. This should explicitly ask for the information required by law.

- Statement of Dispute - The consumer should state that they dispute the debt and are requesting validation. This preserves their rights under the FDCPA.

- Demand to Cease Collection - If sent within the 30-day window, the letter should explicitly demand that the debt collector cease all collection activities until the debt is validated.

- Request for Specific Information - While the law dictates what a collector must provide, the consumer can specifically request details such as the original creditor's name, the original amount, a breakdown of charges, and proof that the collector owns the debt.

- Method of Delivery - It is advisable to send the letter via certified mail with a return receipt requested. This provides proof that the letter was sent and received, which can be important for legal record-keeping.

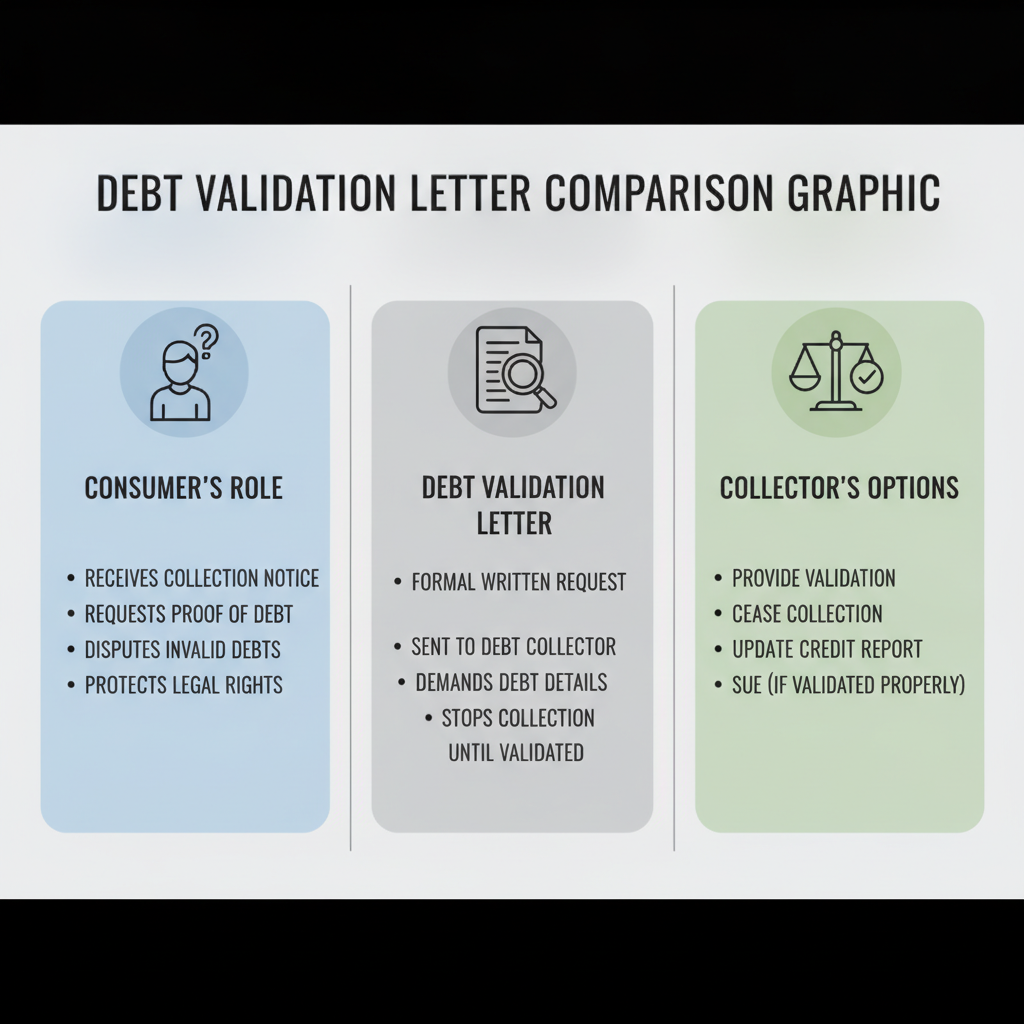

Debt Collector's Response to Validation Request

Upon receiving a timely Debt Validation Letter from a consumer, a debt collector is legally bound by specific actions and restrictions. The response dictates the future course of collection efforts.

- Cessation of Collection - The debt collector must immediately cease all collection activities, including contacting the consumer, until they have provided the requested validation information.

- Provision of Validation Information - The collector must provide the consumer with the required validation information, which includes documentation verifying the debt's existence and their right to collect it. This might include copies of the original credit agreement, payment history, or other relevant records.

- Resumption of Collection - Once the debt collector provides the requested validation information, they may resume collection activities if the information sufficiently validates the debt.

- Inability to Validate - If the debt collector cannot provide adequate validation, they cannot legally continue to pursue collection of that specific debt.

Frequently Asked Questions

Sources

- What information does a debt collector have to give me about a debt they’re trying to collect from me? - Details the required information debt collectors must provide in a validation notice.

- Debt Collection Rule FAQs - Provides comprehensive FAQs on debt collection rules, including validation information requirements.

- Debt collection: Know your rights, avoid scams - Offers guidance on recognizing and dealing with debt collection scams, emphasizing the importance of validation information.

Not the form you're looking for?

Try our legal document generator to create a custom document

Disclaimer: The templates available on this website are provided for general informational purposes only and do not constitute legal advice. They are not intended to be, and should not be interpreted as, compliant with any specific legal, regulatory, or privacy requirements. These templates are not a replacement for professional legal guidance and should not be relied upon for any particular matter or circumstance. Users are strongly encouraged to seek advice from a qualified attorney licensed in their jurisdiction before using, modifying, or relying on any template.

All templates are provided on an "as is," "with all faults," and "as available" basis. The provider disclaims any and all warranties of any kind, whether express, implied, statutory, or otherwise, including without limitation warranties of merchantability, fitness for a particular purpose, title, or non-infringement.

LegalTemplates.com makes no guarantees or representations regarding the accuracy, completeness, expected outcomes, or reliability of the materials contained in these templates or any materials referenced or linked from them.