Debt Collection Dispute Letter

A Debt Collection Dispute Letter is a formal communication instrument used by a consumer to challenge the validity or accuracy of an alleged debt claimed by a debt collector.

Debt Dispute Reason

Select the main reason you are disputing the debt. You can provide further details later.

Provide additional details if you selected 'Other'.

Table of Contents

What is a Debt Collection Dispute Letter?

A Debt Collection Dispute Letter is a formal written communication sent by a consumer to a debt collector to challenge the validity or accuracy of a purported debt. Its primary purpose is to assert a consumer's right to verify a debt and to halt collection activities until such verification is provided. This letter is a critical tool for consumers who believe they do not owe the debt, have already paid it, or whose records do not match the collector's claims.

Purpose and Importance

The act of sending a Debt Collection Dispute Letter serves several important functions in the debt collection process. It formally notifies the debt collector that the consumer questions the debt, triggering specific legal obligations for the collector. Consumers have the right to dispute a debt within 30 days of receiving validation information from a debt collector.

- Verification Request - The letter demands that the debt collector provide specific information, known as validation information, to substantiate the debt.

- Cessation of Collection Activity - If sent within the stipulated timeframe, the letter legally requires the debt collector to cease all collection efforts until they have provided verification of the debt.

- Protection of Consumer Rights - It empowers consumers to exercise their rights under federal consumer protection guidelines, ensuring they are not pressured into paying a debt they may not legitimately owe.

The 30-Day Validation Period

Federal guidance establishes a crucial timeframe during which consumers can dispute a debt and trigger specific collector obligations. This period is initiated when a debt collector first contacts a consumer about a debt.

Debt collectors must provide certain information about the debt, known as validation information, either during their initial communication or within five days of the first contact. This information is essential for consumers to assess the debt and decide whether to dispute it. Key aspects of this period include:

- Information Provided by Collector - Debt collectors are required to provide validation information, including the name of the creditor and the amount owed.

- Consumer's Right to Dispute - Consumers have 30 days from the receipt of this validation information to send a written dispute.

- Impact of Written Dispute - If a consumer sends a written dispute within this 30-day window, the debt collector must stop all collection activity until they provide verification of the debt.

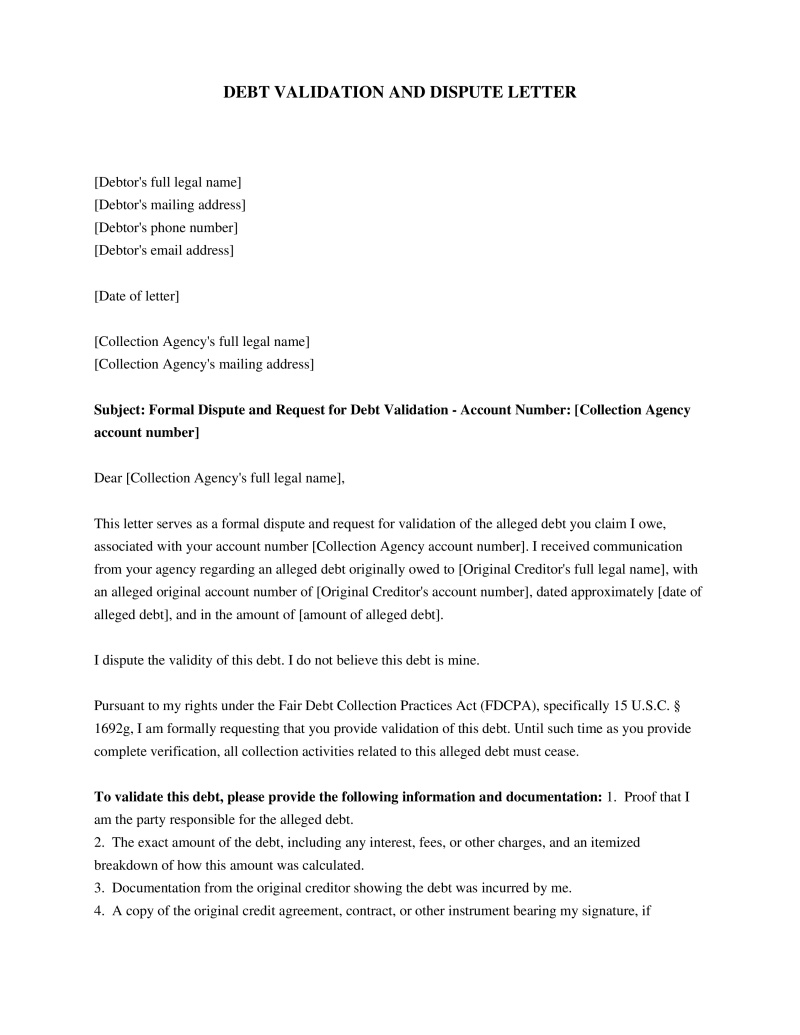

Key Elements of a Dispute Letter

A well-structured Debt Collection Dispute Letter should clearly articulate the consumer's position and request specific information. While there is no single mandated format, effective letters typically include:

- Consumer Identification - Full name, address, and account number(s) associated with the debt, as provided by the collector, to clearly identify the consumer and the debt in question.

- Clear Statement of Dispute - An unequivocal statement that the consumer disputes the debt and is requesting verification.

- Specific Reasons for Dispute - If known, the consumer should state why they are disputing the debt, such as believing it's not theirs, it's already paid, or the amount is incorrect.

- Request for Validation Information - A demand for the debt collector to provide specific validation information, which typically includes: the amount of the debt, the name of the current creditor, and the original creditor.

- Request for Cessation of Activity - A statement requesting that the debt collector cease all collection activities until the debt has been fully verified.

- Date and Signature - The letter must be dated and signed by the consumer.

After Sending the Letter

Once a consumer sends a Debt Collection Dispute Letter, particularly within the 30-day validation period, specific actions are mandated for the debt collector. The process shifts from active collection to verification.

- Collection Activity Stops - The debt collector must immediately cease all collection efforts, including calls and letters, upon receipt of a timely written dispute.

- Verification Process - The collector must then obtain and mail verification of the debt to the consumer. This verification should provide sufficient evidence to confirm the debt's validity and accuracy.

- Resumption of Collection - Collection activities can only resume after the debt collector has sent the requested verification information to the consumer. If verification is not provided, the debt collector cannot continue collection efforts.

Sending the Dispute Letter

The method of sending a Debt Collection Dispute Letter is important to establish a clear record of communication. While any written method is permissible, certain approaches offer better proof of delivery.

To ensure the dispute is properly documented and to protect consumer rights, it is advisable to:

- Send by Certified Mail - This provides a mailing receipt and a return receipt, offering proof that the letter was sent and received by the debt collector.

- Keep Copies - Retain a copy of the letter, all enclosures, and the certified mail receipts for personal records.

- Maintain a Log - Document the date the letter was sent, the date it was received (if a return receipt is obtained), and any subsequent communications from the debt collector.

Frequently Asked Questions

Sources

- What can I do if a debt collector contacts me about a debt I already paid or don't think I owe? - Guidance on disputing debts with debt collectors, including sample letters and steps to take.

- Can a debt collector still collect a debt after I’ve disputed it? - Information on the process and rights after disputing a debt with a collector.

- Debt collection: Know your rights, avoid scams - Consumer advice on dealing with debt collectors, including rights and how to avoid scams.

- Debt Collection FAQs - Frequently asked questions about debt collection practices and consumer rights.

- What information does a debt collector have to give me about a debt they’re trying to collect from me? - Details on the information debt collectors must provide to consumers about debts.

Not the form you're looking for?

Try our legal document generator to create a custom document

Disclaimer: The templates available on this website are provided for general informational purposes only and do not constitute legal advice. They are not intended to be, and should not be interpreted as, compliant with any specific legal, regulatory, or privacy requirements. These templates are not a replacement for professional legal guidance and should not be relied upon for any particular matter or circumstance. Users are strongly encouraged to seek advice from a qualified attorney licensed in their jurisdiction before using, modifying, or relying on any template.

All templates are provided on an "as is," "with all faults," and "as available" basis. The provider disclaims any and all warranties of any kind, whether express, implied, statutory, or otherwise, including without limitation warranties of merchantability, fitness for a particular purpose, title, or non-infringement.

LegalTemplates.com makes no guarantees or representations regarding the accuracy, completeness, expected outcomes, or reliability of the materials contained in these templates or any materials referenced or linked from them.