Gift Letter for Down Payment Template

A Gift Letter for Down Payment is a legal document that formally attests to a financial gift provided for a property's down payment, confirming that no repayment is expected by the donor.

Relationship To Buyer

Select the relationship between the Donor and the Buyer. Lenders often require the relationship to be disclosed.

Provide details if you selected 'Other' above.

Table of Contents

What is a Gift Letter for Down Payment Template?

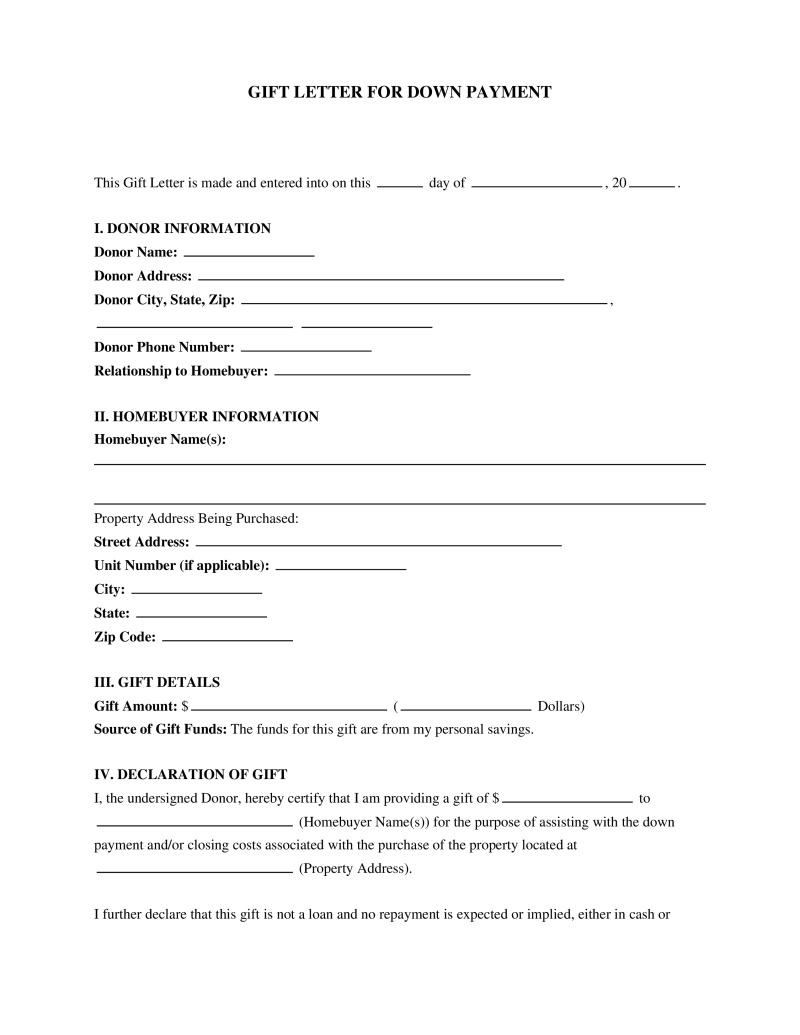

A gift letter for down payment template is a standardized document used in real estate transactions when a portion or the entirety of a homebuyer's down payment is a gift from a third party, typically a family member. This letter formally declares that the funds provided are a true gift, with no expectation of repayment, and are not a loan. Its primary purpose is to satisfy lender requirements, as mortgage lenders need assurance that the down payment funds are not borrowed, which could impact the borrower's debt-to-income ratio and overall financial stability for loan qualification.

Legal Requirements and Validity

The legal validity of a gift letter for a down payment primarily hinges on its clear declaration of a non-repayable gift and the proper identification of all parties involved. Lenders require this document to be legally sound to prevent misrepresentation of a borrower's financial standing. The letter serves as a binding statement from the donor, affirming the nature of the funds.

Key aspects contributing to its legal validity include:

- Clear Intent - The letter must unequivocally state that the funds are a gift, with no obligation for the donee to repay the donor. Any language suggesting a loan or future repayment renders the document invalid for its intended purpose.

- Proper Identification of Parties - Full legal names, current addresses, and contact information for both the donor and the donee must be accurately provided to establish their identities.

- Specific Gift Amount - The exact dollar amount of the gift must be clearly stated, matching the funds transferred for the down payment.

- Source of Funds - Lenders often require documentation proving the origin of the gifted funds, such as bank statements from the donor, to comply with anti-money laundering regulations and ensure the funds are legitimate.

- Donor-Donee Relationship - The letter should specify the relationship between the donor and the donee, as many lenders have policies regarding acceptable gift sources (e.g., immediate family members).

- Signatures and Dates - The donor must sign and date the letter, often with a notarization requirement to attest to the authenticity of the signature and the donor's intent.

Failure to meet these requirements can lead to the lender rejecting the gifted funds, potentially jeopardizing the mortgage approval process.

How to Complete

Completing a gift letter for down payment template involves careful attention to detail to ensure it meets all lender requirements and accurately reflects the nature of the financial gift.

- Identify All Parties Clearly - Begin by accurately listing the full legal names, current addresses, and contact information for both the donor (the individual providing the gift) and the donee (the homebuyer receiving the gift). This ensures proper identification and eliminates ambiguity regarding who is involved in the transaction.

- State the Exact Gift Amount and Purpose - Clearly specify the precise monetary value of the gift in both numerical and written form. Explicitly state that these funds are intended solely for the down payment or closing costs associated with the donee's home purchase, including the property address if known.

- Declare the Gift's Non-Repayable Nature - This is a critical step. The letter must contain unequivocal language stating that the funds are a bona fide gift, with absolutely no expectation or obligation of repayment, either express or implied, from the donee to the donor. This declaration is essential for lender approval.

- Outline the Relationship Between Donor and Donee - Detail the familial or personal relationship between the donor and the donee (e.g., parent, grandparent, sibling, friend). Lenders typically have specific guidelines on who can provide a gift for a down payment, often preferring immediate family members.

- Include Donor's Bank Information and Attestation - The donor should provide the name of the bank from which the funds will be transferred and attest that sufficient funds are available. Lenders will often request bank statements from the donor to verify the source and availability of the funds, ensuring they are legitimate and not borrowed.

- Sign and Date the Document - Both the donor and the donee must sign and date the completed gift letter. In many cases, lenders require the donor's signature to be notarized, adding an extra layer of legal verification and confirming the identity of the signer and the authenticity of their intent.

Required Elements

For a gift letter to be considered valid by mortgage lenders, it must include several essential components that clearly communicate the nature of the financial transaction. Omitting any of these elements can lead to delays or rejection of the mortgage application.

- Date of Letter - The specific date the gift letter is prepared and signed.

- Donor's Full Legal Name and Contact Information - Complete name, address, and phone number of the individual providing the gift.

- Donee's Full Legal Name and Contact Information - Complete name, address, and phone number of the homebuyer receiving the gift.

- Relationship Between Donor and Donee - A clear statement of the familial or personal connection (e.g., "parent," "grandparent," "sibling").

- Exact Gift Amount - The precise dollar amount of the gift, typically written out to prevent discrepancies.

- Property Address - The full address of the property being purchased, if known, to specify the purpose of the funds.

- Statement of No Repayment Obligation - Explicit language confirming the funds are a gift and do not need to be repaid.

- Donor's Source of Funds (often required by lender) - Indication of the bank account from which funds will be drawn.

- Donor's Signature - The legal signature of the individual giving the gift.

- Donee's Signature (sometimes required) - The legal signature of the individual receiving the gift, acknowledging receipt.

- Notary Public Acknowledgment (frequently required) - A notary's seal and signature to verify the donor's signature.

Rights and Obligations

In the context of a gift letter for a down payment, both the donor and the donee assume specific rights and obligations that contribute to the transparency and legality of the transaction.

The donor, as the individual providing the funds, has the primary obligation to:

- Provide a Genuine Gift - The donor must genuinely intend for the funds to be a gift, with no expectation of repayment. Misrepresenting a loan as a gift can lead to legal and financial repercussions.

- Verify Fund Availability - The donor must ensure they have sufficient, legitimate funds available in their accounts to cover the gift amount. Lenders will often request bank statements to confirm this.

- Complete the Gift Letter Accurately - The donor is responsible for providing accurate personal information, stating the correct gift amount, and signing the letter, often requiring notarization, to attest to the truthfulness of the declaration.

- Facilitate Fund Transfer - The donor is obligated to transfer the gifted funds to the donee's account or directly to the closing agent in a timely manner, as instructed by the lender.

The donee, as the homebuyer receiving the funds, has corresponding rights and obligations:

- Right to Utilize Gifted Funds - Once properly documented and transferred, the donee has the right to use the funds for their down payment or closing costs without repayment to the donor.

- Obligation to Disclose Gift - The donee is obligated to fully disclose the gifted funds to their mortgage lender as part of the loan application process. Failure to disclose can be considered mortgage fraud.

- Provide Necessary Documentation - The donee must provide the gift letter and any other requested documentation (e.g., bank statements showing receipt of funds) to their lender.

- Understand Tax Implications - While typically the donor is responsible for gift taxes, the donee should be aware of potential reporting requirements or implications for large gifts.

Both parties share an obligation to act in good faith and ensure the transaction adheres to all legal and lending requirements. Any deviation from the declared intent can have serious consequences for both the mortgage application and potential legal standing.

Federal Regulations and Considerations

Several federal regulations and tax laws influence the process of gifting funds for a down payment, primarily focusing on transparency and preventing illicit financial activities.

Federal considerations include:

- Internal Revenue Service (IRS) Gift Tax - The IRS imposes a gift tax on transfers of property by gift. However, an annual exclusion allows individuals to gift a certain amount each year without incurring gift tax or requiring the donor to file a gift tax return (Form 709). For gifts exceeding this annual exclusion, the donor, not the donee, is generally responsible for reporting the gift and paying any applicable tax, though most gifts are covered by a lifetime exemption (26 U.S.C. § 2503).

- Bank Secrecy Act (BSA) and Anti-Money Laundering (AML) Regulations - These regulations, primarily enforced by the Financial Crimes Enforcement Network (FinCEN), require financial institutions to report suspicious transactions and maintain records of cash transactions exceeding certain thresholds. Mortgage lenders, as financial institutions, must verify the source of large down payment funds, including gifts, to prevent money laundering and terrorist financing (31 U.S.C. § 5311 et seq.).

- Truth in Lending Act (TILA) - While not directly governing gift letters, TILA ensures consumers receive clear information about the terms and costs of credit. Lenders must accurately assess a borrower's ability to repay, and the non-repayable nature of gifted funds directly impacts this assessment by not adding to the borrower's debt load (15 U.S.C. § 1601 et seq.).

- Real Estate Settlement Procedures Act (RESPA) - RESPA aims to protect consumers by requiring disclosures of closing costs and preventing abusive practices in the real estate settlement process. The proper documentation of gifted funds contributes to the transparency of the transaction, ensuring all financial contributions are accounted for at closing (12 U.S.C. § 2601 et seq.).

State-Specific Requirements

While federal laws dictate overarching tax and financial reporting requirements, state laws primarily influence the enforceability and specific notarization requirements of a gift letter for a down payment.

State-specific regulations typically address:

- Notarization Standards - Most states have specific laws governing notary publics, including requirements for identifying signers, administering oaths, and affixing seals. Lenders often require a gift letter to be notarized to authenticate the donor's signature, and these procedures are governed by state notary laws (e.g., California Government Code § 8200 et seq. for notary public duties).

- Statute of Frauds - In some contexts, state Statute of Frauds laws might require certain agreements, especially those related to real estate or significant financial transfers, to be in writing to be enforceable. While a gift letter is not a contract, its written form aligns with the principles of these statutes (e.g., New York General Obligations Law § 5-701).

- Uniform Commercial Code (UCC) - Although primarily concerning commercial transactions, elements of the UCC, particularly those related to negotiable instruments and funds transfers, might indirectly apply to the movement of large sums of money. However, a gift letter itself falls outside the core scope of the UCC as it is not a commercial instrument (e.g., UCC Article 4A - Funds Transfers, adopted by states).

- Consumer Protection Laws - State consumer protection laws may provide avenues for recourse if there is evidence of fraud or misrepresentation in financial transactions, though these are typically broad and not specific to gift letters.

It is important for both donors and donees to be aware that while the core purpose of a gift letter remains consistent, specific procedural requirements, such as notarization details, can vary significantly by state.

Penalties for Non-Compliance

Non-compliance with the requirements for a gift letter for a down payment, particularly through misrepresentation or fraud, can lead to severe penalties for all parties involved.

Potential consequences include:

- Mortgage Fraud - Intentionally misrepresenting a loan as a gift is considered mortgage fraud. Penalties can include significant fines, imprisonment, and a permanent criminal record. Federal law, such as 18 U.S.C. § 1014, specifically prohibits false statements in loan applications to federally insured financial institutions.

- Loan Rejection or Recalling - Lenders have the right to reject a mortgage application if they discover that the gift letter is fraudulent or if the funds are actually a loan. If the fraud is discovered after the loan has closed, the lender may have the right to call the loan due and payable immediately.

- IRS Penalties - If a gift is not properly reported or if gift tax is owed and not paid, the IRS can impose penalties for underpayment, interest on the unpaid tax, and potentially penalties for civil fraud if intent to deceive is proven.

- Legal Action - The donee or donor could face civil lawsuits from the lender or other parties if fraudulent activity results in financial losses.

- Damage to Credit Score - If a loan is recalled due to fraud and the borrower cannot repay, it will severely damage the borrower's credit score, impacting their ability to secure future credit.

The integrity of the gift letter is paramount to the mortgage lending process, and any attempt to circumvent the rules carries substantial risks.

Frequently Asked Questions

Not the form you're looking for?

Try our legal document generator to create a custom document

Disclaimer: The templates available on this website are provided for general informational purposes only and do not constitute legal advice. They are not intended to be, and should not be interpreted as, compliant with any specific legal, regulatory, or privacy requirements. These templates are not a replacement for professional legal guidance and should not be relied upon for any particular matter or circumstance. Users are strongly encouraged to seek advice from a qualified attorney licensed in their jurisdiction before using, modifying, or relying on any template.

All templates are provided on an "as is," "with all faults," and "as available" basis. The provider disclaims any and all warranties of any kind, whether express, implied, statutory, or otherwise, including without limitation warranties of merchantability, fitness for a particular purpose, title, or non-infringement.

LegalTemplates.com makes no guarantees or representations regarding the accuracy, completeness, expected outcomes, or reliability of the materials contained in these templates or any materials referenced or linked from them.