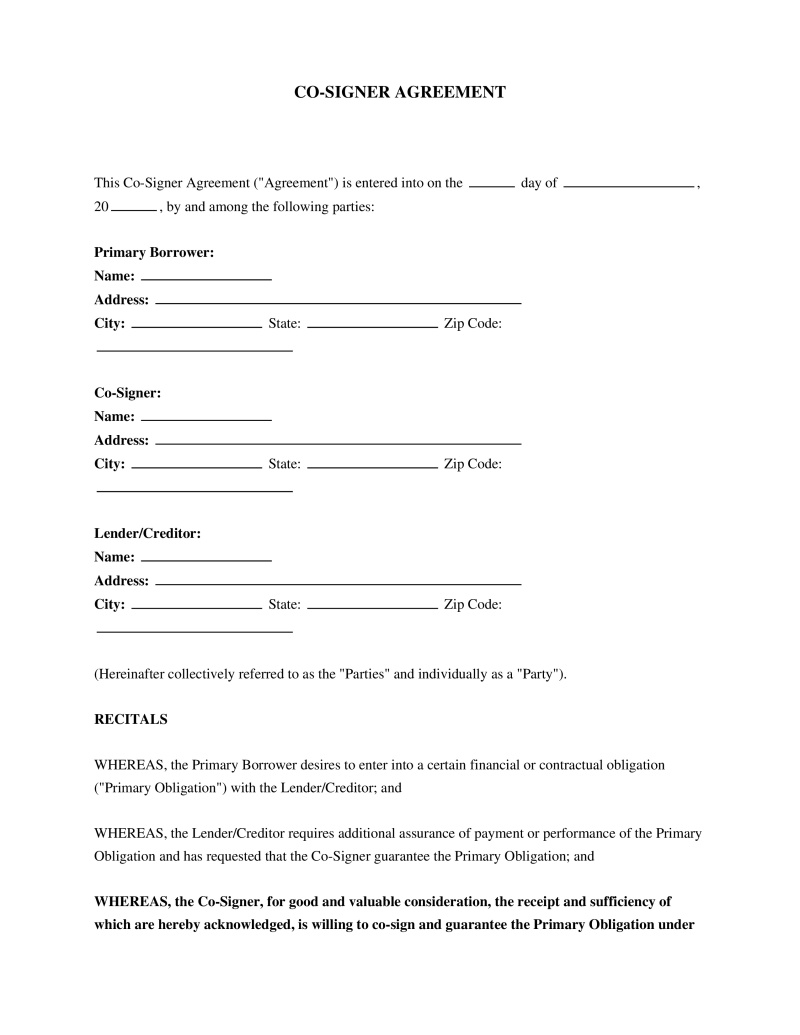

Co-Signer Agreement

A Co-Signer Agreement is a legal contract in which one party, the co-signer, undertakes to guarantee the financial obligations of another party, typically in a lease or loan context.

Obligation Type

Select the primary obligation for which the co-signer is providing assurance.

Provide a brief description of the obligation if you selected 'Other'.

Table of Contents

What is a Co-Signer Agreement?

A Co-Signer Agreement is a legal arrangement where an individual, known as the co-signer, agrees to take on the financial responsibility for a debt or loan if the primary borrower fails to make payments. This agreement is typically sought by lenders when the primary borrower does not meet their creditworthiness criteria, such as having an insufficient credit history or income. The co-signer's commitment provides additional assurance to the creditor, enabling the primary borrower to secure financing they might otherwise be denied.

Understanding the Role of a Co-Signer

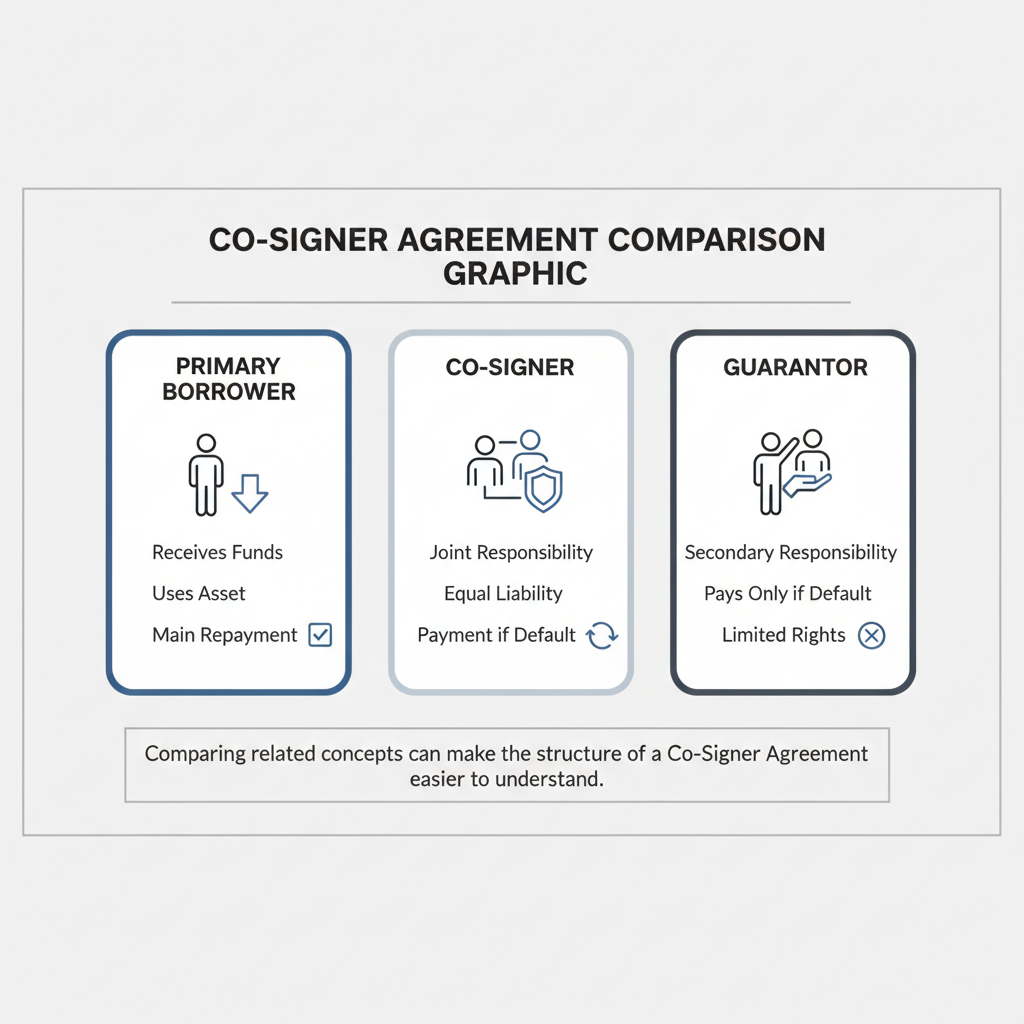

A co-signer is a natural person who formally obligates themselves on a consumer credit transaction without directly receiving the property, services, or money that constitutes the subject of the transaction. This means the co-signer's primary role is to serve as a secondary guarantor of the debt, offering their own credit and financial standing as collateral. Their obligation is typically as binding as that of the primary borrower.

Before a co-signer becomes legally obligated on a consumer credit transaction, creditors are generally required to provide specific disclosures. These disclosures ensure the co-signer fully understands the extent of their financial commitment and the potential consequences should the primary borrower default. The co-signer essentially pledges their credit and assets to back the primary borrower's promise to repay.

When Co-Signing Occurs

Co-signing is a common practice in various financial transactions, often employed when a primary borrower faces challenges in obtaining credit independently. These situations typically arise due to factors that make lenders perceive a higher risk in lending solely to the primary applicant. Common scenarios include:

- Limited Credit History - Young adults or individuals new to credit often lack the established credit history necessary to qualify for loans or leases on their own.

- Low Income or Employment Instability - Lenders may require a co-signer if the primary borrower's income is deemed insufficient to comfortably cover loan payments or if their employment history is unstable.

- Poor Credit Score - Individuals with a low credit score due to past financial difficulties may need a co-signer to mitigate the lender's risk.

- Large Purchases - For significant investments like car loans, mortgages, or student loans, a co-signer can strengthen an application, especially if the loan amount is substantial relative to the primary borrower's financial profile.

Legal Requirements and Disclosures

To protect consumers, specific legal requirements mandate disclosures to co-signers before they become obligated on a credit transaction. These rules aim to ensure that co-signers are fully aware of their responsibilities and the potential financial risks involved. Key requirements include:

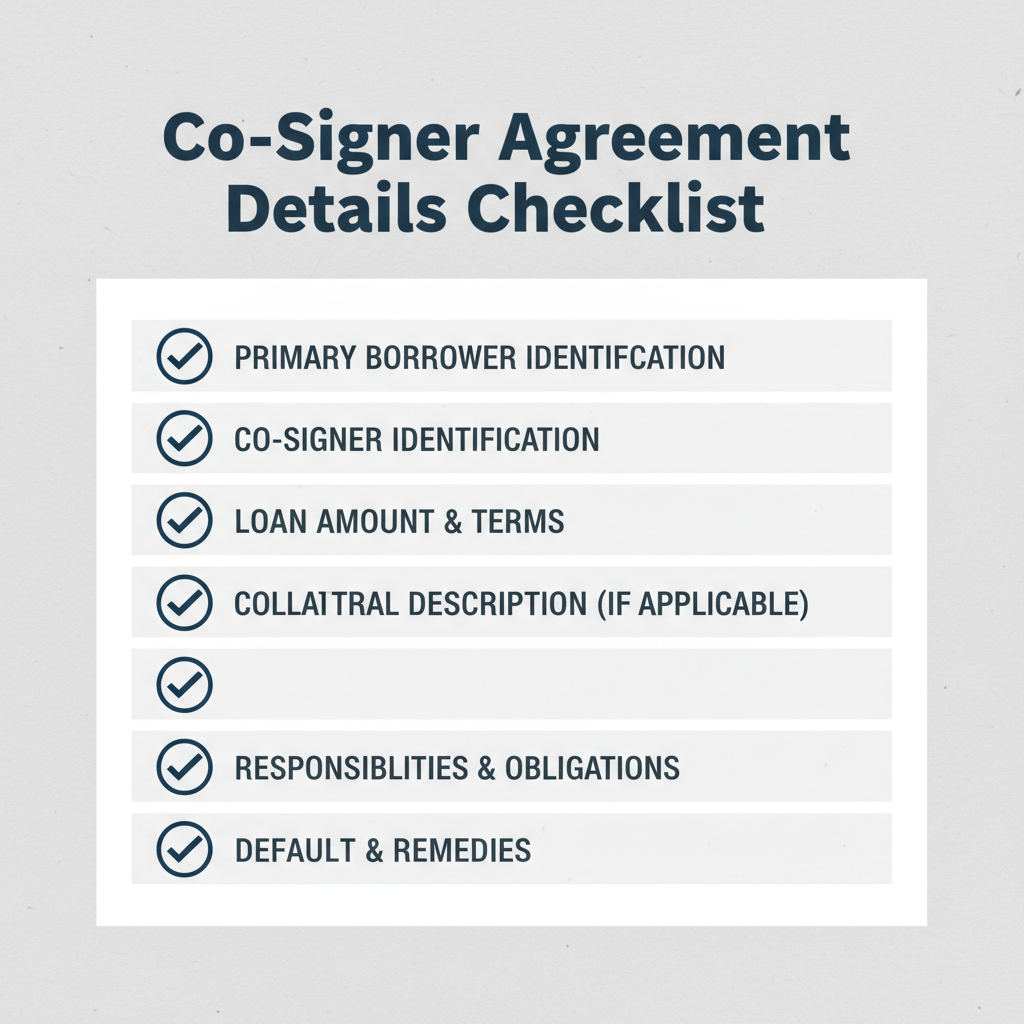

- Definition of Co-Signer - A 'co-signer' is defined as a natural person who becomes obligated on a consumer credit transaction as a co-signer, co-maker, guarantor, endorser, or surety, but does not receive the property, services, or money that is the subject of the transaction (New York General Obligations Law § 15-702).

- Delivery of Documents - Before a co-signer becomes obligated, the creditor must deliver a completed copy of each note, contract, or other writing evidencing the obligation (New York General Obligations Law § 15-702).

- Written Notice of Obligation - Creditors must provide a written notice that identifies the specific debt the co-signer may have to pay and the reason for their potential obligation (New York General Obligations Law § 15-702). This notice explicitly informs the co-signer that they are responsible for paying the loan if the other person fails to pay (Consumer & Business Affairs, LA County).

- Language Consistency - If the transaction is conducted in a language other than English, both the written contract and the required notice provided to the co-signer should also be in that language (Consumer & Business Affairs, LA County).

Risks and Responsibilities for Co-Signers

Co-signing a loan carries significant risks and responsibilities that extend beyond simply lending one's name. A co-signer's obligation is not merely secondary; it is often equal to that of the primary borrower. Understanding these implications is crucial before agreeing to a co-signer agreement.

The primary risk is financial liability. If the primary borrower defaults on payments, the co-signer becomes legally responsible for the entire outstanding debt, including any late fees or collection costs. This obligation can lead to severe financial strain for the co-signer, potentially impacting their savings, assets, and future borrowing capacity. Creditors have the right to pursue the co-signer for payment without first exhausting all collection efforts against the primary borrower.

Furthermore, a co-signed debt appears on the co-signer's credit report. Even if the primary borrower makes all payments on time, the existence of the debt can affect the co-signer's debt-to-income ratio, potentially making it harder for them to obtain new loans or credit themselves. Any missed or late payments by the primary borrower will negatively impact the co-signer's credit score, regardless of the co-signer's own payment history.

Impact on Credit

A co-signer agreement has a direct and often significant impact on the credit profiles of both the primary borrower and the co-signer. For the primary borrower, having a co-signer can enable them to access credit they might not otherwise qualify for, thereby helping them build a positive credit history if payments are made consistently and on time. This can be a crucial step towards financial independence.

For the co-signer, the impact can be more nuanced and potentially negative. The co-signed debt is typically reflected on the co-signer's credit report as if it were their own. This increases their total reported debt, which can lower their credit score or affect their ability to secure other loans, such as a mortgage or car loan, because lenders will consider the co-signed debt as part of their existing financial obligations. Critically, if the primary borrower makes late payments or defaults, the co-signer's credit score will suffer the same negative consequences, regardless of whether the co-signer was aware of the missed payments or had any control over them.

Frequently Asked Questions

Sources

- New York General Obligations Law § 15-702: Co-Signers - Defines 'co-signer' and outlines creditor obligations before a co-signer becomes obligated on a consumer credit transaction.

- Co-Signing a Contract – Consumer & Business Affairs - Provides guidance on the responsibilities and risks of co-signing a contract, including the requirement for a written notice from the seller to the co-signer.

Not the form you're looking for?

Try our legal document generator to create a custom document

Disclaimer: The templates available on this website are provided for general informational purposes only and do not constitute legal advice. They are not intended to be, and should not be interpreted as, compliant with any specific legal, regulatory, or privacy requirements. These templates are not a replacement for professional legal guidance and should not be relied upon for any particular matter or circumstance. Users are strongly encouraged to seek advice from a qualified attorney licensed in their jurisdiction before using, modifying, or relying on any template.

All templates are provided on an "as is," "with all faults," and "as available" basis. The provider disclaims any and all warranties of any kind, whether express, implied, statutory, or otherwise, including without limitation warranties of merchantability, fitness for a particular purpose, title, or non-infringement.

LegalTemplates.com makes no guarantees or representations regarding the accuracy, completeness, expected outcomes, or reliability of the materials contained in these templates or any materials referenced or linked from them.