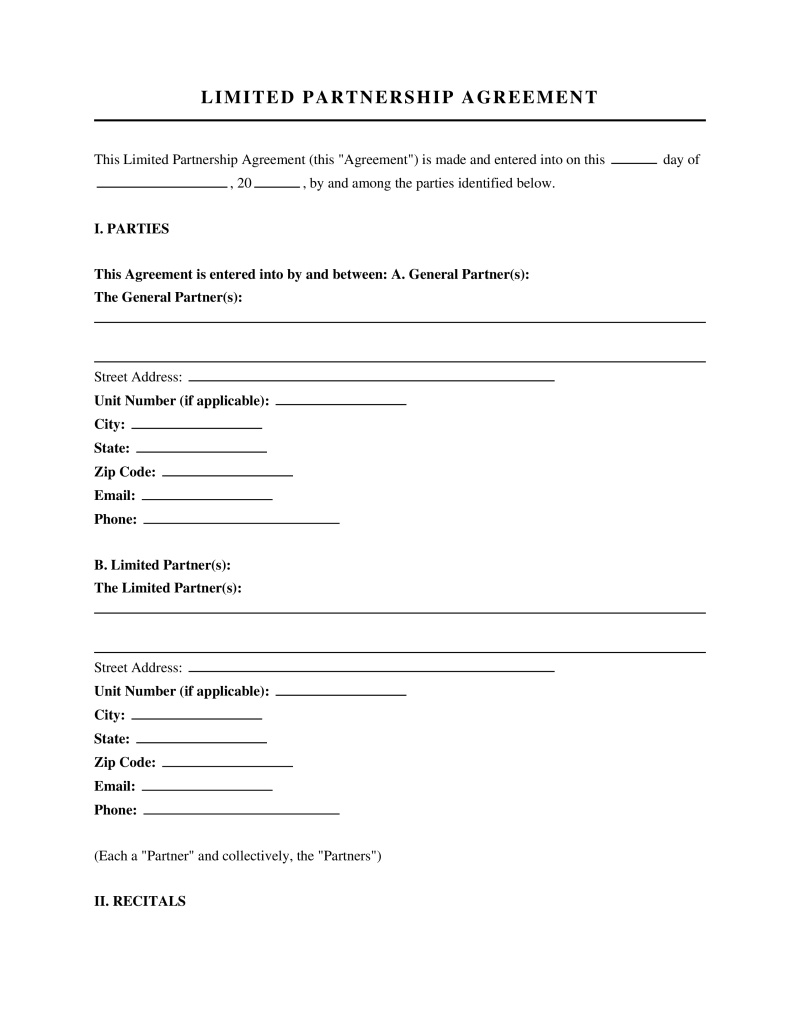

Limited Partnership Agreement

A Limited Partnership Agreement is a legally binding contract that establishes the terms and conditions governing a limited partnership, outlining the rights, responsibilities, and financial contributions of its partners.

Profit Loss Allocation Method

Select the method for allocating profits and losses.

Provide details if allocations differ from capital contributions.

Table of Contents

What is a Limited Partnership Agreement?

A Limited Partnership Agreement (LPA) is a contractual document that establishes the terms and conditions governing a limited partnership. It sets forth the rights, responsibilities, and obligations of both general and limited partners, defining the operational framework of the business. This agreement is crucial for outlining how the partnership will be managed, funded, and dissolved, ensuring clarity among all parties involved. It is executed by the unit holders of a limited partnership to define their respective interests.

Formation and Purpose of the Agreement

The Limited Partnership Agreement serves as the foundational legal document for a limited partnership, detailing its structure and operational rules. While the formal establishment of a limited partnership often involves filing a Certificate of Limited Partnership with a state authority, the LPA provides the internal governance framework. The agreement is a critical tool for preventing disputes by clearly defining roles, contributions, and expectations from the outset.

For instance, to form a domestic limited partnership in New York, a Certificate of Limited Partnership must be filed with the Department of State, accompanied by a filing fee. This official filing creates the entity, but the LPA dictates its internal workings. Within 120 days after filing, a limited partnership in New York is also required to publish a copy of its Certificate of Limited Partnership in two newspapers designated by the county clerk.

Parties to the Limited Partnership Agreement

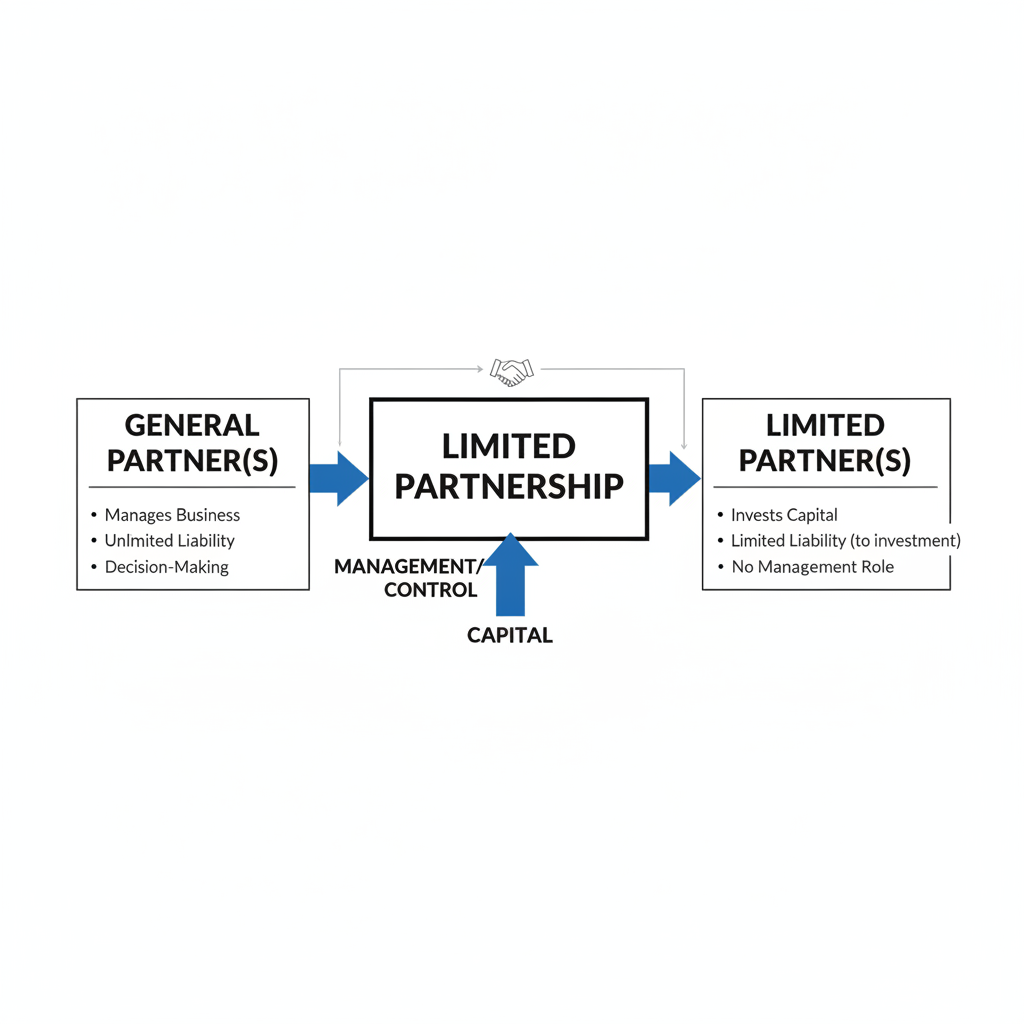

A limited partnership, and consequently its agreement, involves two distinct types of partners, each with different levels of involvement and liability. The agreement meticulously defines the roles, responsibilities, and liabilities for each type, which is fundamental to the limited partnership structure.

- General Partner(s) - These partners are responsible for the management and control of the partnership's business. They have exclusive control over the management and investment decisions of the partnership. General partners typically bear unlimited personal liability for the partnership's debts and obligations, meaning their personal assets can be at risk.

- Limited Partner(s) - These partners contribute capital to the partnership but do not participate in its day-to-day management or investment decisions. Their liability is generally limited to the amount of capital they have invested in the partnership, protecting their personal assets from partnership debts. The unit holders of a limited partnership will execute documents that set forth the rights and restrictions applicable to interests in the partnership.

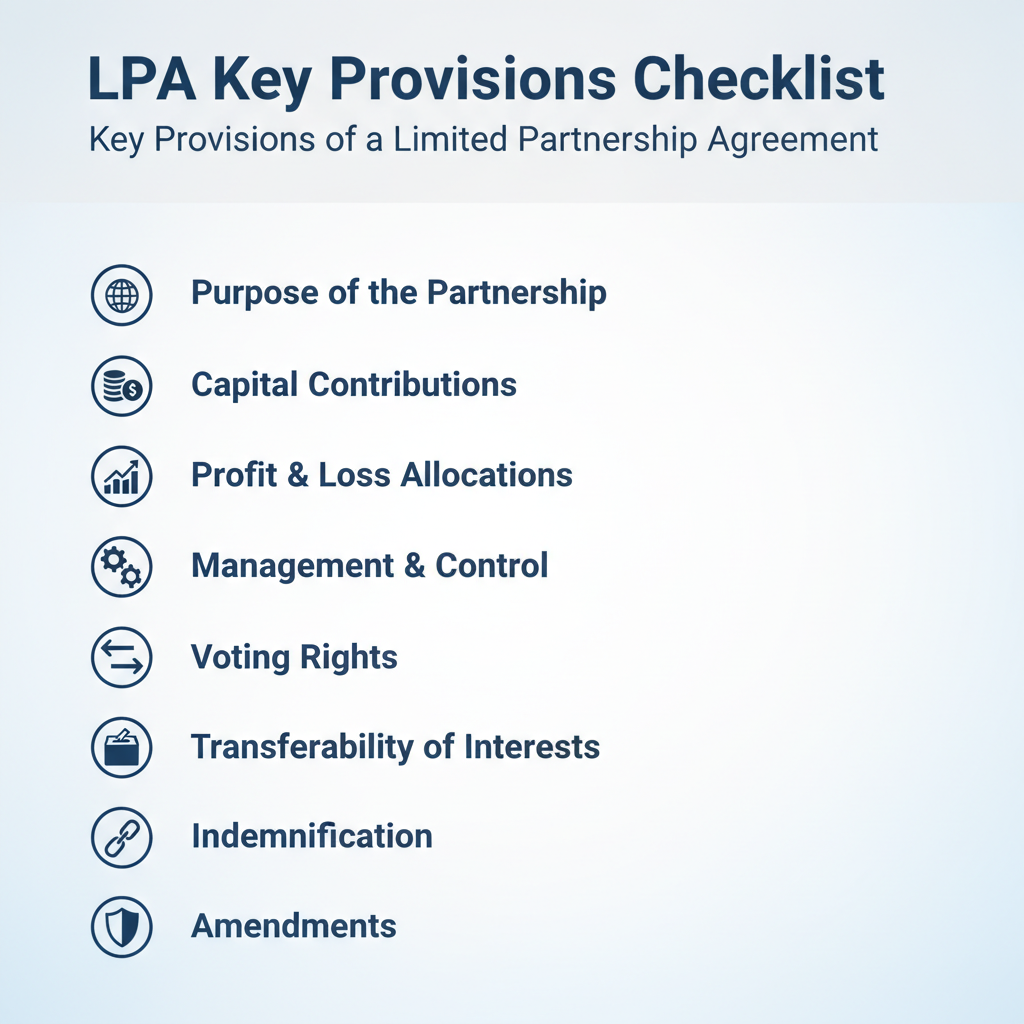

Key Provisions of a Limited Partnership Agreement

A comprehensive Limited Partnership Agreement typically includes several essential provisions that govern the partnership's operations, finances, and governance. These clauses ensure that all partners understand their roles and the partnership's operational guidelines.

- Purpose of the Partnership - Clearly defines the business activities and objectives the limited partnership will undertake.

- Capital Contributions - Specifies the initial and any subsequent capital contributions required from both general and limited partners, including the form these contributions may take (cash, property, services).

- Profit and Loss Allocations - Details how the partnership's profits and losses will be allocated among the partners, often proportional to capital contributions but can be structured differently.

- Distributions - Outlines the timing and methods for distributing cash or other assets to partners, distinguishing between regular distributions and those upon dissolution.

- Management and Control - Defines the powers and responsibilities of the general partner(s) in managing the business, and explicitly states the limited partners' lack of management authority.

- Voting Rights - Specifies any matters on which limited partners may have voting rights, which are typically limited to major decisions such as amending the agreement or selling substantial assets.

- Transferability of Interests - Sets forth the rules and restrictions regarding the transfer, sale, or assignment of a partner's interest in the partnership.

- Dissolution and Liquidation - Establishes the conditions under which the partnership may be dissolved and the procedures for liquidating its assets and distributing proceeds.

- Indemnification - Provisions for protecting partners from liabilities incurred in the course of partnership business, subject to certain conditions.

- Amendments - Procedures for modifying the Limited Partnership Agreement, typically requiring the consent of a majority or all partners.

Management and Decision-Making

Central to the structure of a limited partnership is the clear delineation of management authority. The Limited Partnership Agreement explicitly vests the general partner with control over the partnership's operations and strategic decisions. This concentration of power in the general partner is a defining characteristic that distinguishes limited partnerships from other business structures.

The general partner has exclusive control over the management and investment decisions of the partnership. Limited partners, by contrast, have no right to participate in management or investment decisions. Their role is primarily that of passive investors. Any involvement by limited partners in the management of the business could risk their limited liability status, potentially exposing them to the same unlimited liability as a general partner.

Financial Contributions and Distributions

The financial aspects of a limited partnership are meticulously detailed within the Limited Partnership Agreement, covering how capital is raised and how returns are distributed. This section ensures transparency and fairness regarding the economic participation of all partners.

- Capital Contributions - Partners commit capital, which can be in the form of cash, property, or services, as specified in the agreement. These contributions form the financial basis of the partnership's operations.

- Allocation of Profits and Losses - The LPA defines the method for allocating partnership profits and losses among the general and limited partners. This allocation may be proportionate to capital contributions or based on other agreed-upon formulas.

- Distributions - The agreement outlines the conditions, frequency, and amounts of distributions to partners. These distributions represent a return on their investment and are typically made from available cash flow after operational expenses and reserves.

Transferability of Partnership Interests

The ability to transfer or assign a partner's interest in a limited partnership is a significant aspect addressed in the Limited Partnership Agreement. These provisions are designed to protect the partnership's stability and ensure that new partners meet specific criteria. The unit holders of a limited partnership will execute documents that set forth the rights and restrictions applicable to interests in the partnership, including transfer rights.

Typically, LPAs include clauses that restrict the free transferability of limited partnership interests. These restrictions might include requiring the consent of the general partner or other limited partners, or granting existing partners a right of first refusal. Such provisions are common to maintain control over who becomes a partner and to prevent unintended changes in the partnership's composition.

Frequently Asked Questions

Sources

- Certificate of Limited Partnership for Domestic Limited Partnership - Provides information on forming a domestic limited partnership in New York, including filing requirements and fees.

- Domestic Limited Partnerships - Offers comprehensive details on domestic limited partnerships in New York, including formation, amendments, and publication requirements.

- IRS Private Letter Ruling 200111038 - Discusses the general purpose and structure of a limited partnership, including management and distribution provisions.

- IRS Private Letter Ruling 200348006 - Details the rights and restrictions applicable to interests in a limited partnership, including transfer rights and obligations.

- IRS Exempt Organizations-Technical Instruction Program for FY 2003 - Provides an overview of the partnership agreement, including its purpose and key provisions.

Not the form you're looking for?

Try our legal document generator to create a custom document

Disclaimer: The templates available on this website are provided for general informational purposes only and do not constitute legal advice. They are not intended to be, and should not be interpreted as, compliant with any specific legal, regulatory, or privacy requirements. These templates are not a replacement for professional legal guidance and should not be relied upon for any particular matter or circumstance. Users are strongly encouraged to seek advice from a qualified attorney licensed in their jurisdiction before using, modifying, or relying on any template.

All templates are provided on an "as is," "with all faults," and "as available" basis. The provider disclaims any and all warranties of any kind, whether express, implied, statutory, or otherwise, including without limitation warranties of merchantability, fitness for a particular purpose, title, or non-infringement.

LegalTemplates.com makes no guarantees or representations regarding the accuracy, completeness, expected outcomes, or reliability of the materials contained in these templates or any materials referenced or linked from them.