Promissory Note

Create Promissory Note

Promissory Note

A Promissory Note is a legal instrument that embodies a written promise by one party to pay a specified sum of money to another party, either on demand or at a predetermined future date.

Answer the question(s) below to create your Promissory Note

Repayment Type

A demand note is payable upon request by the Lender. An installment note is repaid over time according to a schedule.

Table of Contents

What is a Promissory Note?

A promissory note is a written promise made by one party (the maker or promisor) to pay a specified sum of money to another party (the payee or promisee) at a future date or on demand. This legally binding document outlines the terms of a debt, serving as a formal acknowledgment of a financial obligation. Promissory notes are commonly used in various loan agreements, ranging from personal loans between individuals to more complex business transactions and student financing, such as those within the Federal Perkins Loan Program (34 CFR § 674.31; U.S. Courts Glossary).

Key Characteristics of a Promissory Note

A promissory note functions as a standalone financial instrument, detailing the specific conditions under which a debt is incurred and will be repaid. Its enforceability stems from its clear articulation of a promise to pay, making it a valuable tool for both lenders and borrowers seeking to formalize financial arrangements. Understanding these characteristics is crucial for anyone entering into a loan agreement involving such a note.

- Unconditional Promise - The note must contain an unconditional promise to pay a definite sum of money. Conditions that might make the payment uncertain could invalidate the note.

- Specific Amount - The exact principal amount of the loan must be clearly stated in the document.

- Payable on Demand or at a Definite Time - Payment must be due either immediately upon the payee's request or on a specific future date or series of dates.

- Signed by the Maker - The individual or entity promising to pay must sign the note, signifying their acceptance of the obligation.

- Payable to Order or Bearer - The note specifies to whom the payment is due, either a named person or entity (to order) or whoever holds the note (to bearer).

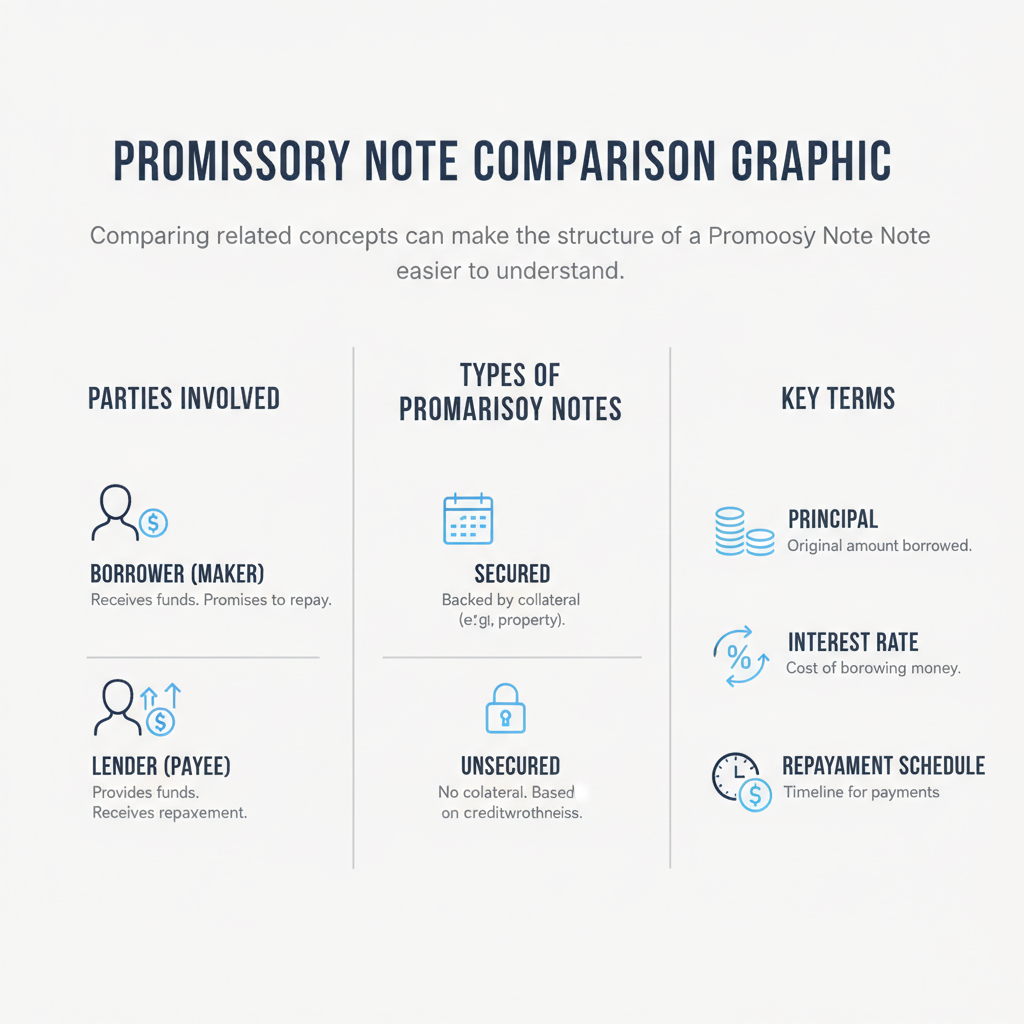

Types of Promissory Notes

Promissory notes come in various forms, each tailored to different financial scenarios and repayment structures. The type of note selected depends on the nature of the loan, the relationship between the parties, and the desired terms of repayment.

- Simple Promissory Note - This is the most basic form, typically used for straightforward loans between individuals or for small business loans. It usually specifies a lump sum payment due on a particular date or on demand, often without complex interest calculations or collateral.

- Demand Promissory Note - With this type, the maker agrees to pay the specified amount whenever the payee demands it. There is no fixed repayment schedule or maturity date; the lender can call for repayment at any time.

- Installment Promissory Note - This note outlines a schedule of regular payments, including both principal and interest, over a set period until the loan is fully repaid. It is common for mortgages, car loans, and student loans.

- Secured Promissory Note - A secured note involves collateral, meaning the borrower pledges an asset (like a car or property) to the lender. If the borrower defaults, the lender can seize the collateral to recover the outstanding debt.

- Unsecured Promissory Note - This note is not backed by any collateral. The lender relies solely on the borrower's creditworthiness and promise to repay. Personal loans and many business loans are often unsecured.

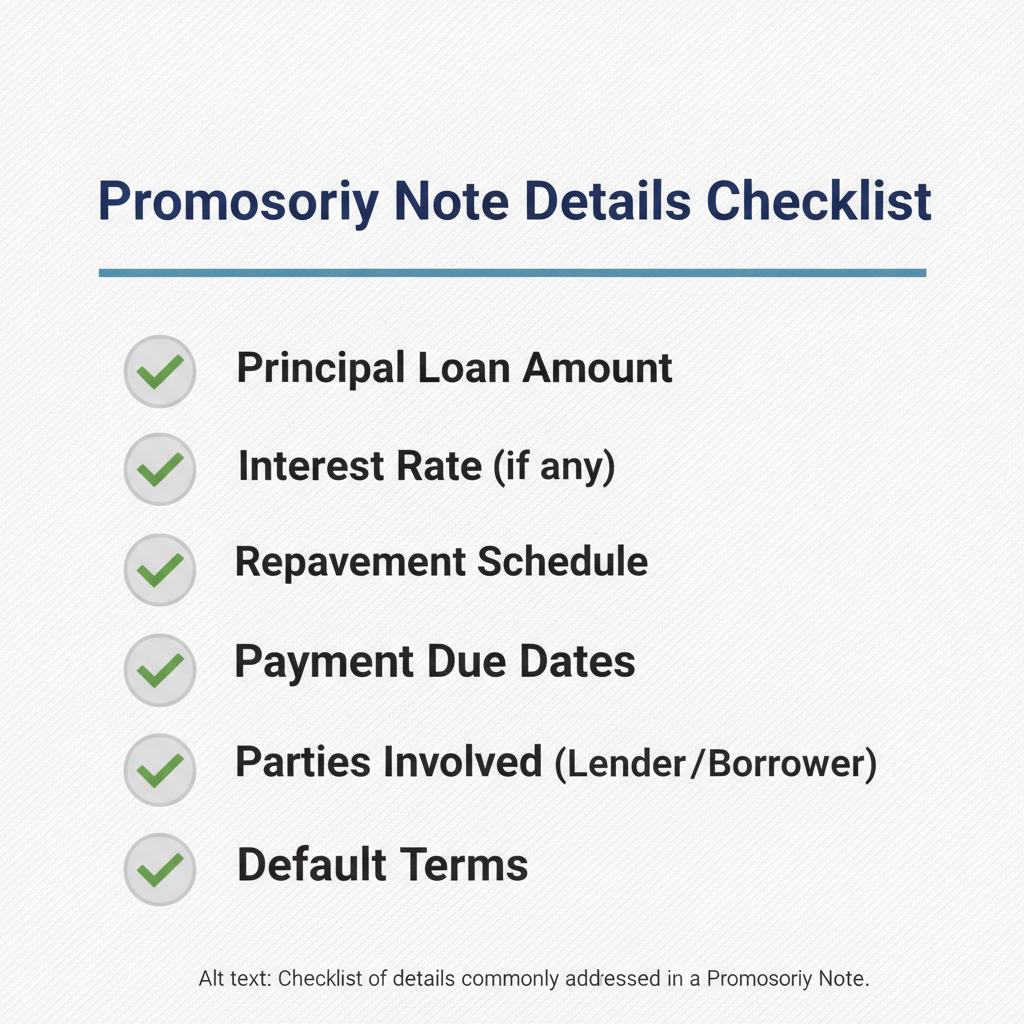

Essential Elements of a Promissory Note

For a promissory note to be legally sound and enforceable, it must contain several key pieces of information. These elements ensure clarity regarding the terms of the debt and the responsibilities of each party involved.

- Principal Amount - The total sum of money being borrowed.

- Parties Involved - The full legal names and addresses of both the maker (borrower) and the payee (lender).

- Interest Rate - If applicable, the annual percentage rate (APR) at which interest will accrue on the principal.

- Payment Schedule - Details on how and when payments will be made, including due dates, payment frequency (e.g., monthly, quarterly), and the total number of payments.

- Maturity Date - The date by which the entire loan, including any interest, must be fully repaid.

- Terms of Default - Conditions that constitute a default (e.g., missed payments) and the consequences thereof, such as acceleration of the loan or penalties.

- Signatures - The signature of the maker is always required. Depending on local laws or the parties' agreement, witness signatures or notarization may also be included for added enforceability.

- Date of Execution - The date on which the promissory note is created and signed.

Usage and Applications

Promissory notes are versatile instruments used in a wide array of financial transactions, providing a structured way to document loans. Their flexibility allows them to be adapted for both formal institutional lending and informal agreements.

- Personal Loans - Often used between friends, family members, or individuals for private loans, providing a formal record of the debt and repayment terms.

- Business Loans - Businesses use promissory notes when borrowing from banks, private lenders, or even from their owners or other businesses. They can be part of larger financing agreements or for smaller, specific needs.

- Real Estate - While a mortgage secures a loan with real property, the underlying debt obligation is often documented by a promissory note. The note specifies the amount borrowed and repayment terms, while the mortgage provides the collateral.

- Student Loans - Many educational loans, including federal programs like the Perkins Loan Program, require students to sign a promissory note, committing them to repay the borrowed funds (34 CFR § 674.31).

- Vehicle Loans - Similar to real estate, a promissory note documents the loan amount and repayment schedule for vehicle purchases, with the vehicle often serving as collateral.

Distinction from Other Financial Documents

While a promissory note is a fundamental document in lending, it is important to distinguish it from other related financial instruments that serve different, albeit sometimes complementary, purposes. Misunderstanding these differences can lead to confusion regarding rights and obligations.

- Loan Agreement - A loan agreement is typically a more comprehensive document than a promissory note. It often includes additional clauses detailing covenants, representations, warranties, conditions precedent, and default remedies beyond the basic promise to pay. A promissory note can be an exhibit to or incorporated within a larger loan agreement.

- Mortgage - A mortgage is a security instrument that pledges real property as collateral for a loan. It does not, by itself, represent the promise to pay the debt; rather, it secures the debt that is typically evidenced by a separate promissory note. The note creates the personal obligation, while the mortgage creates a lien on the property.

- I.O.U. - An I.O.U. (meaning "I Owe You") is an informal acknowledgment of a debt. It typically states the amount owed and the parties involved but lacks the detailed terms of repayment, interest, or consequences of default found in a promissory note. An I.O.U. is usually not a legally enforceable promise to pay in the same way a promissory note is.

Frequently Asked Questions

The primary purpose is to serve as a written, legally binding promise by one party to pay a specific sum of money to another party. It formalizes a debt obligation and outlines the terms of repayment.

Yes, a promissory note can often be transferred to another party, especially if it is made payable "to order" or "to bearer." This transfer typically involves endorsement and delivery, making the new holder the payee.

If a borrower defaults on a promissory note by failing to meet the agreed-upon payment terms, the lender can pursue legal action to recover the outstanding debt. The specific remedies available depend on the terms outlined in the note and applicable laws.

While not always legally mandated for every informal loan, a promissory note is highly recommended for any significant loan to clearly document the terms and protect both the lender and borrower. It provides legal recourse if disputes arise.

Generally, a promissory note does not legally require notarization to be valid, but notarization can add an extra layer of authenticity and make it more difficult for a party to deny their signature. Some lenders or specific circumstances may require it.

A secured promissory note is backed by collateral, meaning an asset is pledged by the borrower that the lender can seize upon default. An unsecured promissory note is not backed by collateral, relying solely on the borrower's promise to repay and creditworthiness.

Sources

- 34 CFR § 674.31 - Promissory note. - Defines the term 'promissory note' within the context of the Federal Perkins Loan Program.

- Glossary of Legal Terms - Provides definitions of legal terms, including 'promissory note'.

Related Documents

Forms commonly used with Promissory Note.

Not the form you're looking for?

Try our legal document generator to create a custom document

Disclaimer: The templates available on this website are provided for general informational purposes only and do not constitute legal advice. They are not intended to be, and should not be interpreted as, compliant with any specific legal, regulatory, or privacy requirements. These templates are not a replacement for professional legal guidance and should not be relied upon for any particular matter or circumstance. Users are strongly encouraged to seek advice from a qualified attorney licensed in their jurisdiction before using, modifying, or relying on any template.

All templates are provided on an "as is," "with all faults," and "as available" basis. The provider disclaims any and all warranties of any kind, whether express, implied, statutory, or otherwise, including without limitation warranties of merchantability, fitness for a particular purpose, title, or non-infringement.

LegalTemplates.com makes no guarantees or representations regarding the accuracy, completeness, expected outcomes, or reliability of the materials contained in these templates or any materials referenced or linked from them.